Turkiye: Imported ferrous scrap market slow amid limited activities w-o-w; Scrap-Rebar spread over $200/t

...

The imported ferrous scrap market in Turkiye remained relatively busy this week, as the country's severe economic conditions continue to weigh on consumer sentiment, which has markedly worsened this month. Despite the regular summer season of lower company activity, the movement of economic indices exposes underlying structural concerns in the Turkish economy. These problems have ramifications for steel suppliers as well.

Furthermore, the rise in energy costs since August has further destabilised steel producers. The price difference between rebar and scrap in Turkiye has recently fallen to $192/t, the lowest in three years, but again touched the $200-205/t level due to a hike in rebar prices from major steelmakers up to $580-590/t FOB, reflecting an increase from the $580-585/t FOB range reported a week earlier.

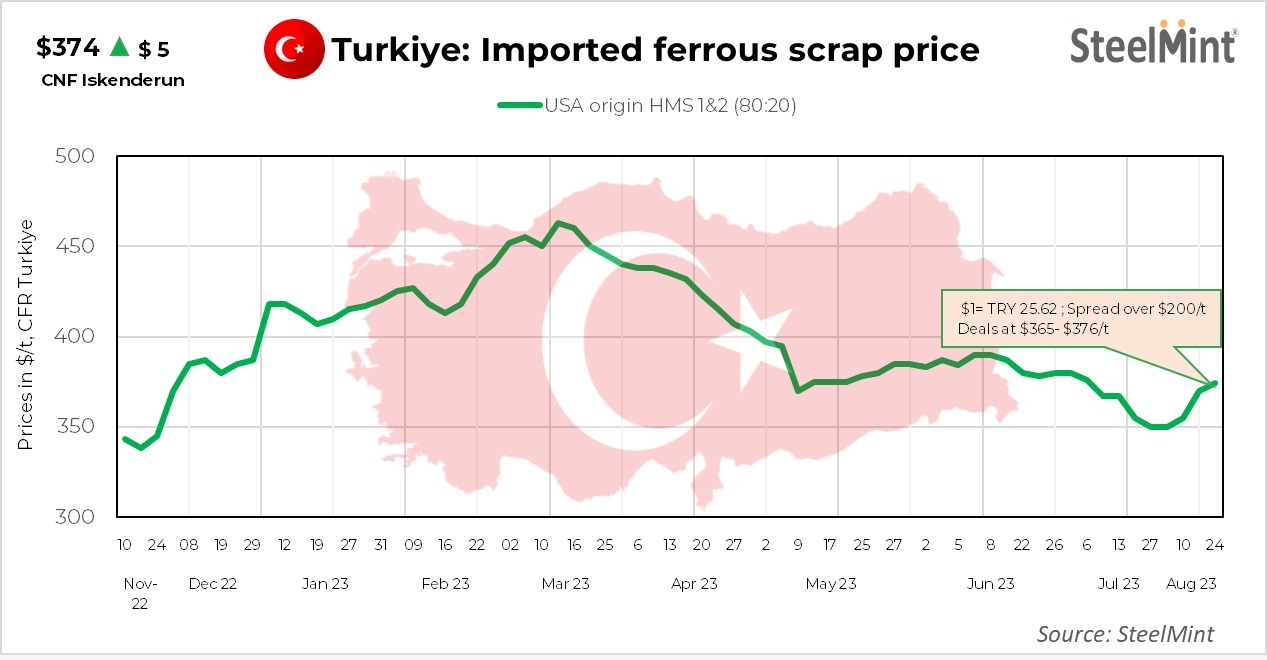

US-origin bulk HMS 1&2 (80:20) prices are slightly up by $5/t w-o-w to $370-374/t CFR, up $20-24/t from last month's $351/t.

Meanwhile, Turkish rebar producers largely increased their export offer prices as domestic sales began to pick up despite demand in the export market for Turkish rebar remains slow.

The depreciation of the exchange rate has negatively impacted the import market, necessitating compensation through the export market. However, the rebar export market remains sluggish, with stiff competition from neighboring countries like Saudi Arabia.

The main concern revolves around weak demand for rebar, as the mills grapple with the need to offset elevated operational expenses within the long steel prices. Unfortunately, both local and overseas customers are reluctant to accept these price hikes.

Recent deals:

- A US-origin bulk cargo with HMS(80:20) and Shredded booked by a west Marmara-based mill at $374/t and $394/t respectively on a CFR Turkiye basis.

- A European supplier sold a bulk cargo at $369/t to a Marmara-based mill on a CFR Turkiye basis.

- A west Marmara-based mill booked HMS (80:20) cargo from the US at $370/t on a CFR basis.

- An Aegean region-based mill acquired bulk cargo with HMS (80:20) at $371.5/t CFR Turkiye.

- A West Black Sea region mill captured HMS (90:10) another US cargo from the same seller at $376.50/t on a CFR Turkiye basis.

- A West-Marmara-based mill has reportedly booked 35,000 t of mix scrap from Europe. These include 25,000 t of HMS (80:20) at $365/t, 5,000 t of bonus scrap at $385/t CFR, and 5,000 t shredded scrap at $390/t CFR.

Domestic market-

Presently, the profitability of rebar production is notably constrained due to prevailing market prices. To ensure profitability, Turkish steelmakers are opting to prioritise cost-effective domestic scrap sources over more expensive imports. One strategy under consideration involves increasing the selling prices of rebar to attain a viable profit margin. However, this approach raises apprehensions about potential sales reduction.

Kardemir sales: On the domestic front, Turkish integrated mill Kardemir initiated a fresh round of rebar sales targeting local customers. The company implemented a price increase of $40/t (TRY 1,024/t ) compared to the previous trading campaign two weeks ago, setting the new price at $595/t (TRY 15,232/t) EXW. Kardemir successfully sold 20,000 of the product on the same day.

Other Turkish producers of domestic rebar have followed a similar pricing trend, with price hikes of $10-15/t observed since the middle of the previous week. This brings the local price range to $585-600/t EXW, contingent on the specific region. The price escalation predominantly stems from elevated production costs and ongoing depreciation of the lira, as demand continues to fall short of expectations.

Metallics imports to Turkiye go down in H1: Turkish importers of pig iron and hot briquetted iron (HBI) made significant reductions in their intake of these raw materials in June. This shift has led to a reversal in the upward trend observed year-to-date. Despite this change, the sourcing locations for these materials remained consistent: Russia continued to be the primary supplier of pig iron, while the United States remained the top source for HBI shipments. In the first half of 2023, Turkey imported a total of 711,739 tons of pig iron, marking an 8% decline compared to the same period the previous year. These figures were reported by the Turkish Statistical Institute (TUIK).

Wire Rod Imports Outpace Exports in Turkey during H1: The initial half of 2023 witnessed a notable disparity between wire rod imports and exports in Turkey. Local wire rod producers experienced a significant decline in their export activities from January to June. Although Russia retained its role as the primary supplier, Asia emerged as the largest source of wire rod imports among various regions. According to data from the Turkish Statistical Institute (TUIK), Turkey's wire rod exports for H1 2023 totalled 239,674 tons, reflecting a substantial 59.2% decrease compared to the previous year. Local mills exhibited reduced trade with their traditional partners during this period.

The Turkish lira stood at TRY 25.57 against the greenback slightly strengthened yet weak due to the slow export market.

Outlook: As per market forecast, it appears that the Turkish scrap market will struggle to recover from this stagnant state unless broader economic challenges. But suppliers anticipating a better demand in September which might face volatility in different origin deals.