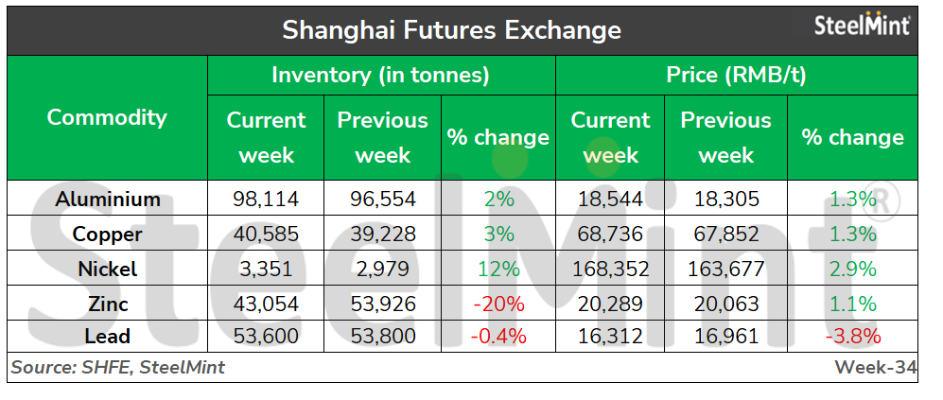

China: SHFE base metal inventory exhibits mixed trend w-o-w

The latest weekly inventory report from the Shanghai Futures Exchange (SHFE) reveals a diverse trend in inventory levels. With the exception of zinc and lead, all other c...

The latest weekly inventory report from the Shanghai Futures Exchange (SHFE) reveals a diverse trend in inventory levels. With the exception of zinc and lead, all other commodities have experienced an increase in warehouse inventory alongside a rise in futures.

China, a major player in the global metal sector, is currently grappling with the challenges of an economic slowdown, which poses a significant threat to the demand for global commodities. In response, Chinese authorities have recently unveiled a comprehensive work plan aimed at developing the building material industry, as part of their efforts to prioritize stable economic growth within the country.

The primary objective of this work plan is to boost domestic mining of nonferrous metals, with a particular focus on strategic minerals such as copper, aluminium, nickel, lithium, and platinum metals.

To achieve this, seven Chinese government departments, including the Ministry of Industry and Information Technology (MIIT), have jointly issued a detailed plan that aims to promote and ensure the steady growth of the non-ferrous metal industry.

The ultimate goal is to achieve a y-o-y industrial increase of 5.5% in 2023. Additionally, the plan seeks to expedite domestic exploration and utilization of strategic metals that are currently in short supply, such as copper, nickel, and lithium.

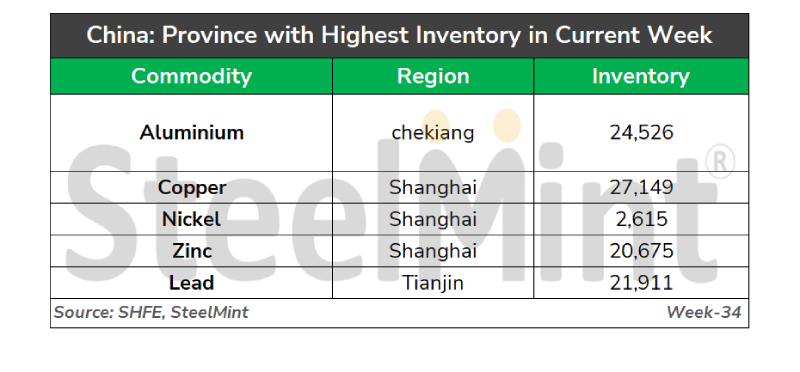

Commodity-wise inventories

Aluminium

In SHFE warehouses, aluminium inventories increased slightly by 2% w-o-w. Total inventories were assessed at 98,114 t, down from 96,554 t last week. SHFE aluminium futures surged by 1.3% w-o-w to RMB 18,544/t ($2,544/t). The influx of imported aluminium was strong resulting in a slight hike in the warehouse inventory levels.

Copper

Copper stocks in SHFE warehouses increased to 40,585 t this week from 39,228 t last week. Similarly, copper futures increased by 1.3% w-o-w to RMB 68,736/t ($9,430/t). The downstream buyers purchased material on a need basis due to rising prices in the futures market.

Nickel

Nickel stocks rebounded this week to 3,351 t from last week’s 2,979 t. Nickel prices moved up by 2.9% w-o-w to RMB 168,352/t ($23,096/t) compared to RMB 163,667/t ($22,453/t) last week. The demand from buyers was weak due to accumulated inventory from the last few weeks and high SHFE prices.

Zinc

Zinc inventories in major SHFE warehouses fell significantly by 20% w-o-w. Currently, the inventory stands at 43,054 t compared to 53,926 t last week. Meanwhile, future prices slipped by 1.1% w-o-w to RMB 20,289/t ($2,783/t). Due to tight supply and increasing demand leads to a fall in inventories.

Lead

Lead inventories remained rangebound, reaching 53,600 t against last week’s 53,800 t. Lead future prices slipped by 3.8% w-o-w to RMB 16,312/t ($2,238/t).